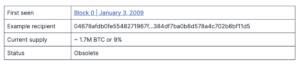

As anxiety grows around every new twist and turn in the ongoing QuadrigaCX drama, along with extensive QuadrigaCX media coverage, Canada’s mainstream media has been calling on the government to bring in better oversight and regulation of cryptocurrency businesses, especially cryptocurrency exchanges.

In response to these calls for more regulation and calls from some crypto businesses for more regulatory clarity, the Canadian Securities Administrators (CSA) and the Investment Industry Regulatory Organization of Canada (IIROC) released a discussion paper on March 14, 2019, with a “New Proposed Platform Framework” that would aim to specifically tailor regulations to the special risks posed by cryptocurrency exchanges.

The CSA consultation paper, which can be viewed here, asks 22 questions and requests comments from crypto/fintech companies, market participants/investors and other crypto stakeholders about what regulations would best fit in the unique new cryptocurrency marketplace.

When Is a Crypto Exchange a Securities or Derivatives Dealer?

As a number of observers have commented, this round of consultations is mainly about how to define the new business of cryptocurrency exchanges and how far to go in imposing old regulatory models on a new economic system.

Calgary-based securities and cryptocurrency lawyer Matt Burgoyne commented on Twitter:

“There is a lot to unpack in the new CSA consultation paper on cryptocurrency exchanges. Exchanges must consider whether their interactions with users create a derivative contract or futures contract.”

He added, “Non-security tokens trading on Canadian exchanges may be derivatives and still subject to regulation … this is a really detailed set of consultation questions, comments from industry due May 15.”

Lawyer Evan Thomas, who headed up a legal team at Osler, Hoskin & Harcourt LLP to produce a summary of the CSA consultation paper, told Bitcoin Magazine:

“A big issue with this proposal is that it is not clear as a legal matter that Canadian securities regulators have jurisdiction to regulate platforms for trading bitcoin and other crypto-assets that are not securities.”

One of the goals stated in the Osler paper is:

“To ensure that the CSA does not exceed its jurisdiction over the cryptoasset industry, we are hopeful that Platform regulation will provide further clarity regarding types of cryptoassets and related services that are not subject to securities regulation, such as tokens that are not investment contracts or derivatives and non-custodial cryptocurrency wallets.”

Third Time Lucky?

The Canadian government has conducted two previous consultation rounds with the cryptocurrency industry (in 2014 and 2018) but Thomas, who is cautiously optimistic, notes that this new initiative is a more direct response to cases like that of QuadrigaCX.

“Earlier regulation was directed at combating money laundering and terrorist financing. This proposed framework is motivated by investor protection concerns; that is, trying to protect crypto users who use custodial exchanges from risks like hacking, embezzlement and market manipulation,” Thomas explained.

The ghost of QuadrigaCX can be seen in the current discussion paper which asks: What operational requirements should be put in place to prevent a collapse like that of QuadrigaCX? What measures can affect market integrity, fair pricing, disclosure of conflict of interest and business continuity planning?

Would the Proposed Regulations Have Prevented the QuadrigaCX Collapse?

It’s an interesting question whether the proposed regulations in the discussion paper would have prevented what happened at QuadrigaCX — and the answer is likely no.

Amber D. Scott, CEO of Outlier Canada, a cryptocurrency compliance consulting company, told Bitcoin Magazine that without adequate enforcement resources, it’s unlikely the new rules would have affected the outcome.

“Background checks for beneficial owners and executives are useful if they are sufficiently in-depth and acted upon. The QuadrigaCX story is interesting because they were registered with FINTRAC (Financial Transactions and Reports Analysis Centre of Canada) at one point (though it’s not clear whether they were up front in their application about the beneficial owners).

“Similarly, proposed audits are useful tools, but I expect that fooling auditors would be possible, especially given that there will be very few experienced auditors that also understand crypto assets at this stage.”

She added that, in many cases, the impact is likely to be a greater cost of compliance burden for companies that choose to operate within these frameworks, and very little for those that do not. “In my estimation, some of the most important (and lacking) resources are those needed to investigate and prosecute bad actors. Fraud is already illegal.”

Clear Regulations Are Good for Crypto Business

Despite this, a number of Canadian crypto exchanges, including Coinsquare and Coinberry, have said they would welcome clear, fair regulations that make it easier to be compliant and will help bring them into the financial mainstream.

The Osler paper highlights the positive benefits of regulation including better relationships with the banking sector:

“By establishing a regulatory regime for Platforms, the Framework may make it easier for Platforms to obtain and maintain commercial relationships with banks and other financial institutions, which remains an ongoing challenge for certain Platforms.”

In addition, clear regulations that apply to crypto asset securities dealers would be an opening for businesses that are currently flying under the radar.

“The Framework potentially opens the door for Platforms that transact in cryptoassets that are securities or derivatives to operate within Canada in a compliant manner. Examples may include Platforms dealing in security tokens or tokenized assets, decentralized prediction markets or other so-called ‘decentralized finance’ (DeFi) activities.”

The proposed regulations will apply to crypto platforms located in Canada, as well as foreign platforms with Canadian participants, which might be eligible for exemptions if they are appropriately regulated in their home jurisdiction.

The CSA is a federal government agency coordinating financial regulations for Canadian capital markets and IIROC is the industry’s self-regulatory organization that oversees investment dealers in Canada’s debt and equity markets.

Comments are due by May 15, 2019.

This article originally appeared on Bitcoin Magazine.